April Monthly Market Review

- May 14

- 4 min read

Global markets moved higher in April as improving sentiment around the Middle East and continued strength in technology and semiconductor sectors supported equity returns. However, inflation reaccelerated across major economies due to rising energy prices, prompting central banks to maintain a cautious “higher for longer” stance on interest rates. While growth-oriented equity markets performed strongly, bond markets came under pressure as rising yields weighed on fixed income assets.

Growth Leads, Bonds Lag as Inflation Pressures Rebuild Across Global Markets Firm

Central banks hold rates as inflation re-accelerates on energy-driven pressures from the Middle East

Technology and semiconductor-driven markets surge, with Korea and Finland leading performance

Bond markets struggle as yields rise, while investors rotate toward growth and regional opportunities

In-line with broader markets, the Balanced portfolio benchmark returned 3.52% in April, buoyed by renewed prospects of peace in the Middle East.

Inflation and Interest Rates.

UK.

In April 2026, the Bank of England adopted an “active hold,” keeping Bank Rate at 3.75% in an 8–1 vote, with one member pushing for a hike amid rising energy‑driven risks. Policymakers emphasised that the Iran conflict had materially increased uncertainty and could yet necessitate “forceful” tightening if inflation proved persistent.

Inflation, meanwhile, re-accelerated, with CPI rising to 3.30% in March and expected to climb further as higher oil and gas prices feed through, reversing earlier disinflation.

U.S. Federal Reserve.

In April 2026, the Federal Reserve held rates at 3.75%, extending its pause amid persistent inflation and heightened uncertainty linked to the Iran conflict. Notably, the decision was unusually divided, with multiple dissents highlighting concern that policy may need to remain restrictive, or even tighten, if price pressures persist.

Inflation then reaccelerated, with CPI rising from 3.30% in March to 3.80% in April, driven primarily by surging energy costs. This marked the highest reading in nearly three years and reinforced expectations of a prolonged higher for longer rate backdrop.

European Central Bank (ECB).

In April 2026, the European Central Bank held its key rates unchanged, keeping the deposit rate at 2.00% as policymakers balanced rising inflation against weakening growth. The decision reflected a clear wait and see stance, with officials highlighting intensifying upside risks to inflation, downside risks to growth, and maintaining a data dependent approach.

Inflation, meanwhile, reaccelerated, with euro area CPI rising from 2.60% in March to 3.00% in April, driven primarily by surging energy costs. This pushed inflation back above target and reinforced expectations that the ECB may need to tighten policy, despite an increasingly fragile growth backdrop.

Market performance.

Developed markets.

Finland’s equity market was the standout performer, rising +11.25% and leading developed markets over the period. The strength is consistent with the market’s sector composition, which is heavily weighted toward financials (27%), industrials (22%), and technology (16%). These sectors are typically more leveraged to global growth and risk sentiment, meaning they tend to outperform during periods of improving equity momentum.

In contrast, Norway was the weakest performer, declining ‑3.91% and standing apart as the only negative market in the ranking. This underperformance reflects the structure of the Norwegian market, as it is one of the most commodity-sensitive developed markets, which were challenged last month.

Emerging Markets.

Korea was the standout performer, surging +34.14% and decisively outperforming all other emerging markets. The rally is consistent with Korea’s heavy technology sector exposure, particularly semiconductors, which play a dominant role in the index. This concentration in high‑growth, export-oriented sectors provides a clear structural explanation for Korea’s outsized return relative to more domestically driven peers.

In contrast, Indonesia was the weakest performer, falling -9.97% and underperforming the broader emerging market universe. The Indonesian market has a meaningful tilt toward commodities and domestic cyclicals, including energy, materials and financials, leaving it more exposed to shifts in commodity prices and local economic conditions.

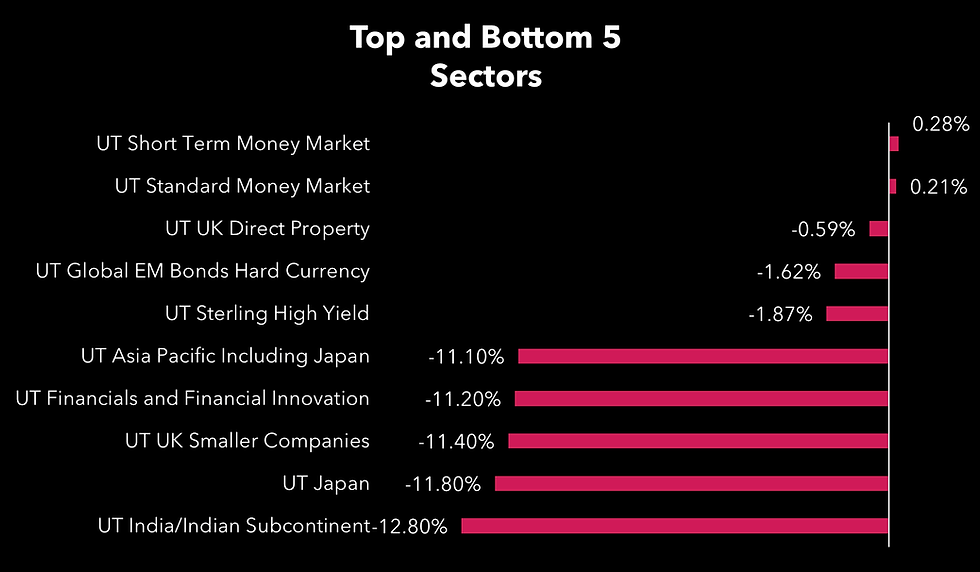

Sector performance.

Technology was the clear standout performer, returning +24.32% and comfortably leading all other sectors over the period shown. The move is consistent with the powerful AI- and semiconductor-led rally seen across global equity markets, with Reuters reporting that the S&P 500 and Nasdaq hit record highs in early May as investors piled into Nvidia, Micron and other AI-linked names, while the Philadelphia Semiconductor Index surged on the back of strong demand for AI data-centre infrastructure.

In contrast, UK Index Linked Gilts was the weakest performer, declining -1.31% and finishing at the bottom of the sector table. The weakness fits with the difficult backdrop for UK government bonds more broadly, where yields moved sharply higher as investors reacted to a combination of persistent inflation concerns, fiscal uncertainty and political instability.

Source: FE FundInfo, 14/05/26

Summary.

Global markets showed a mixed but more resilient tone over the period, with performance increasingly shaped by a combination of renewed inflation pressures and strong equity momentum. Inflation re-accelerated across major economies, driven primarily by higher energy costs linked to the Middle East conflict, pushing CPI higher in the UK, US and euro area. In response, central banks maintained a “higher for longer” stance, holding rates steady but signalling a willingness to tighten further if inflation proves persistent.

Equity market performance diverged significantly. Developed markets were led by Finland, supported by its cyclical and growth-oriented sector exposure, while Norway lagged, reflecting weakness in commodity-sensitive markets. In emerging markets, Korea delivered exceptional returns, driven by its heavy exposure to semiconductors and technology, while more commodity- and domestically focused markets such as Indonesia underperformed.

At the sector level, technology was the dominant driver of returns, benefiting from continued strength in artificial intelligence and semiconductor demand, which pushed global indices to new highs. In contrast, fixed income sectors struggled, particularly UK index-linked gilts, as rising nominal and real yields weighed on bond prices amid persistent inflation and fiscal uncertainty.

The overall environment reflects a clear shift in market leadership, with investors favouring growth and innovation themes while remaining cautious on interest rate-sensitive assets. Although policy remains on hold, the combination of elevated inflation and geopolitical uncertainty continues to shape asset allocation and market dynamics.

Sources.

The ‘Balanced portfolio benchmark’ is the UT Mixed Investment 20-60% Shares Sector.

Bank of England holds rates and spells out inflation risks from Iran war, RTE 30th April 2026

Bank of England Monetary Policy Report - April 2026, Bank of England

Tradingeconomics.com, March 2026 https://www.istockphoto.com/