March Monthly Market Review

- Apr 8

- 4 min read

Global markets came under significant pressure in March as geopolitical tensions in the Middle East triggered a sharp surge in energy prices, reigniting inflation concerns across major economies. Central banks in the UK, US and eurozone responded by holding interest rates steady, balancing persistent inflation against growing economic uncertainty. Investor sentiment deteriorated, driving a broad risk-off move in equities, while capital flowed into safer assets such as money markets. Performance across regions diverged sharply, with energy-exporting markets benefiting from higher oil prices, while more globally exposed and technology-heavy markets experienced steep declines.

Markets Adjust as Policy Holds Firm

UK, US and ECB hold steady as inflation jumps on Middle East–driven energy spikes

Norway and Colombia soar on oil strength while Sweden and Korea plunge amid risk‑off selling

Money markets outperform as geopolitical tensions send investors fleeing to cash

In-line with broader markets, the Balanced portfolio benchmark returned -4.97% in March.

Inflation and Interest Rates.

UK.

UK interest rates were unanimously held at 3.75% in March 2026 as the Bank of England paused policy amid surging energy prices linked to the Middle East conflict. Inflation pressures intensified, with UK grocery inflation stuck at 4.30% in March, signalling rising food and fuel costs, while broader CPI hovered near 3.00% in February.

U.S. Federal Reserve.

U.S. interest rates were held at 3.75% in March 2026 as the Federal Reserve paused policy amid elevated inflation, slowing job gains and uncertainty from the Iran conflict. Inflation remained stubborn: headline CPI hovered around 2.40% year‑on‑year in February, while producer prices and energy‑driven pressures signalled renewed upside risks.

European Central Bank (ECB).

EU interest rates remained unchanged in March 2026, with the ECB holding its key rates steady at it’s the 19 March meeting amid Middle East–driven uncertainty. The current ECB deposit rate is 2.00%, a level most economists expect to persist through 2026.

Inflation, however, jumped sharply. Eurozone headline inflation rose to 2.50% in March, up from 1.90% in February, driven almost entirely by an energy shock linked to the Iran conflict, pushing it above the ECB’s 2.00% target.

Market performance.

Developed markets.

MSCI Norway (+11.61%)

Norway’s equity market stood out as a rare bright spot in an otherwise risk‑off month. Broader global equities fell sharply in March due to escalating geopolitical tensions and surging oil prices, but energy‑heavy markets like Norway benefited from the sharp rise in crude, with Brent up more than 60% during the month.

MSCI Sweden (‑11.60%)

In contrast, Sweden was among the hardest‑hit developed markets. Global risk aversion weighed heavily on European equities, with Sweden experiencing notable declines as markets reacted to geopolitical instability, higher bond yields, and weaker sentiment across non‑energy sectors.

Emerging Markets.

MSCI Colombia (+10.35%)

Colombia stood out as the strongest performer among emerging markets in March. This rebound coincided with improving sentiment linked to geopolitical easing, including rising hopes that the reopening of the Strait of Hormuz would stabilise global energy markets, particularly supportive for Colombia’s oil‑sensitive equities.

MSCI Korea (‑24.00%)

South Korea was the worst‑performing emerging market, driven by a dramatic sell‑off in March as the Iran‑related conflict triggered a surge in oil prices and global risk aversion. Foreign outflows intensified this downturn, with overseas investors selling a record 35.9 trillion won of Korean equities. High‑valuation sectors, particularly semiconductors (Samsung Electronics and SK Hynix), experienced heavy declines due to both geopolitical pressure and technology‑specific headwinds (e.g., concerns over Google’s new memory‑efficient AI architecture reducing chip demand).

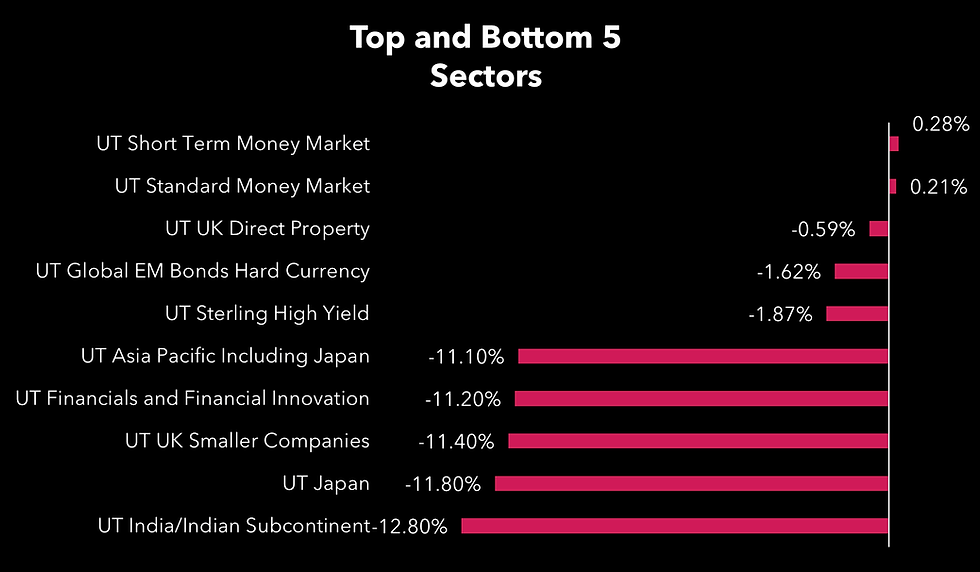

Sector performance.

UT Short‑Term Money Market (+0.28%) & UT Standard Money Market (+0.21%)

Money market sectors were the month’s strongest performers, benefiting from a flight to safety as global geopolitical tensions escalated sharply following the Middle East conflict beginning on 28th February.

UT India/Indian Subcontinent (12.8%)

Regions highly exposed to energy imports and global volatility suffered heavily in March. Emerging markets experienced their worst monthly decline since 2020, driven by war related oil shocks that disrupted supply chains and elevated inflation expectations.

Source: FE FundInfo, 02/04/26

Summary.

Global markets weakened in March as energy-driven inflation surged following the Middle East conflict. Central banks in the UK, US and eurozone held rates steady, but rising fuel and food costs pushed inflation higher, particularly in Europe. Equity performance was highly uneven: energy rich Norway and Colombia gained sharply, while Sweden and Korea fell amid risk aversion and heavy outflows. Money market sectors proved the month’s strongest performers as investors sought safety. The Balanced portfolio benchmark declined 4.97%, reflecting the sharp shift in sentiment and heightened geopolitical uncertainty.

Sources.

The ‘Balanced portfolio benchmark’ is the UT Mixed Investment 20-60% Shares Sector.

Bank Rate maintained at 3.75% - March 2026 Monetary Policy, March 2026

UK Grocery Inflation Sticks at 4.3% in March, Says Worldpanel, by Reuters, 31/03/26

Fed votes to hold rates steady, notes ‘uncertain’ impacts from Iran war, by Jeff Cox, CNBC, 18/03/26

U.S. Inflation Insight: March 2026, Mar 11, 2026 – By Chris Harrison and Tim Cooper, MNI

Tradingeconomics.com, March 2026 https://www.istockphoto.com/