CleverAdviser

CleverAdviser

Strong start for US markets

- US manufacturing grows

- Commodities lose steam

- State support sees China rally

It was a positive month for the Balanced portfolio benchmark which returned 0.61% in February, led by Equity market gains. Although the market is certain of interest rate cuts, there is still great uncertainty around their timing and so the Fixed Income markets continue to oscillate, with UK Gilts down 1.43% for the month.

Inflation and Interest rates.

Bank of England

Inflation in the UK remained unchanged at 4.00%, below market expectations of 4.20%.

Bank of England (BoE) Governor Andrew Bailey told MPs that policymakers were looking for progress on services prices, wage growth and the labour market before they felt they could begin reducing interest rate. However, Bailey said it’s “not unreasonable” for the markets to expect the Bank to cut interest rates this year. He told the Treasury Select Committee “It’s the progress of those three things. We don’t need inflation to come back to target before we cut interest rates, I must be very clear on that, that’s not necessary.”

US Federal Reserve

The annual inflation rate in the US fell back to 3.10% in January 2024 following a brief increase to 3.40% in December but came higher than forecasts of 2.90%.

U.S. Federal Reserve Chair Jerome Powell told U.S. lawmakers that he and his colleagues would “keep our heads down” in a charged presidential election year, with interest rate cuts still likely in coming months, but only if warranted by further evidence of falling inflation.

Rate cuts “really will depend on the path of the economy. Our focus is on maximum employment and price stability, and the incoming data as they affect the outlook, and those are the things we’ll be looking at,” Powell told the House Financial Services Committee. We are just going to keep our heads down and do our jobs and try to deliver what the public is expecting from us.”

European Central Bank

Inflation in the EU fell to 2.60% in February, down from 2.80% for the prior month.

Policymakers said that Euro zone inflation is heading back towards the 2% target, but the European Central Bank (ECB) still needs more confirmation before it can cut rates.“The latest data confirms the ongoing disinflation process and is expected to bring us gradually further down over 2024,” said ECB President Christine Lagarde. That message was echoed by Spanish central bank Governor Pablo Hernandez de Cos, who said the next move was a cut but there was no hurry.

“The next move in interest rates is going to be a cut,” de Cos said in Madrid. “We are not being explicit on when that will happen, I think there is some time left for that, but it is important to underline that the ECB’s target is the 2% symmetric target.”

If the ECB moved too quickly, inflation could rise again which might force the ECB into tightening again, a costly back and forth, Lagarde warned.

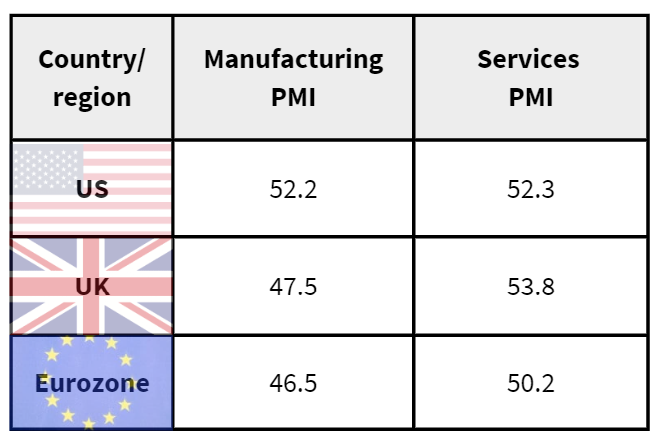

Note: Less than 50 PMI = contraction and more than 50 PMI = growth

Manufacturing

In February 2024, the US manufacturing sector experienced its swiftest expansion since July 2022. Output rose significantly, and total new orders grew at the strongest pace in 21 months. Notably, new export orders expanded for the first time in three months.

The UK manufacturing PMI reached its highest level in ten months (47.5), despite ongoing contraction for the 19th consecutive month. The Red Sea crisis disrupted production and vendor delivery schedules, leading manufacturers to seek alternative suppliers at higher costs from closer markets. Weak demand resulted in declining new order intakes.

In the Eurozone, the manufacturing PMI improved to 46.5, signalling the second-slowest deterioration since March 2023. Germany drove the overall decline, while softer contractions were observed in the Netherlands, Italy, and France. Spain returned to growth, and Greece and Ireland recorded their best expansions in 24 and 20 months, respectively.

Services

In February 2024, the US services sector showed solid performance, with output rising for the thirteenth successive month. New business inflows increased, albeit at a slower pace due to a contraction in foreign business. Pressure on capacity decreased as backlogs of work fell, supported by a rise in employment.

In the UK, service providers experienced steady business activity driven by upticks in new orders and modest employment growth. Output remained strong, slightly below January’s eight-month high.

The Eurozone saw a small expansion in the services sector after seven months. Activity levels rose, demand stabilised, and new business contracted more slowly. Service sector employment also improved, reaching an eight-month high.

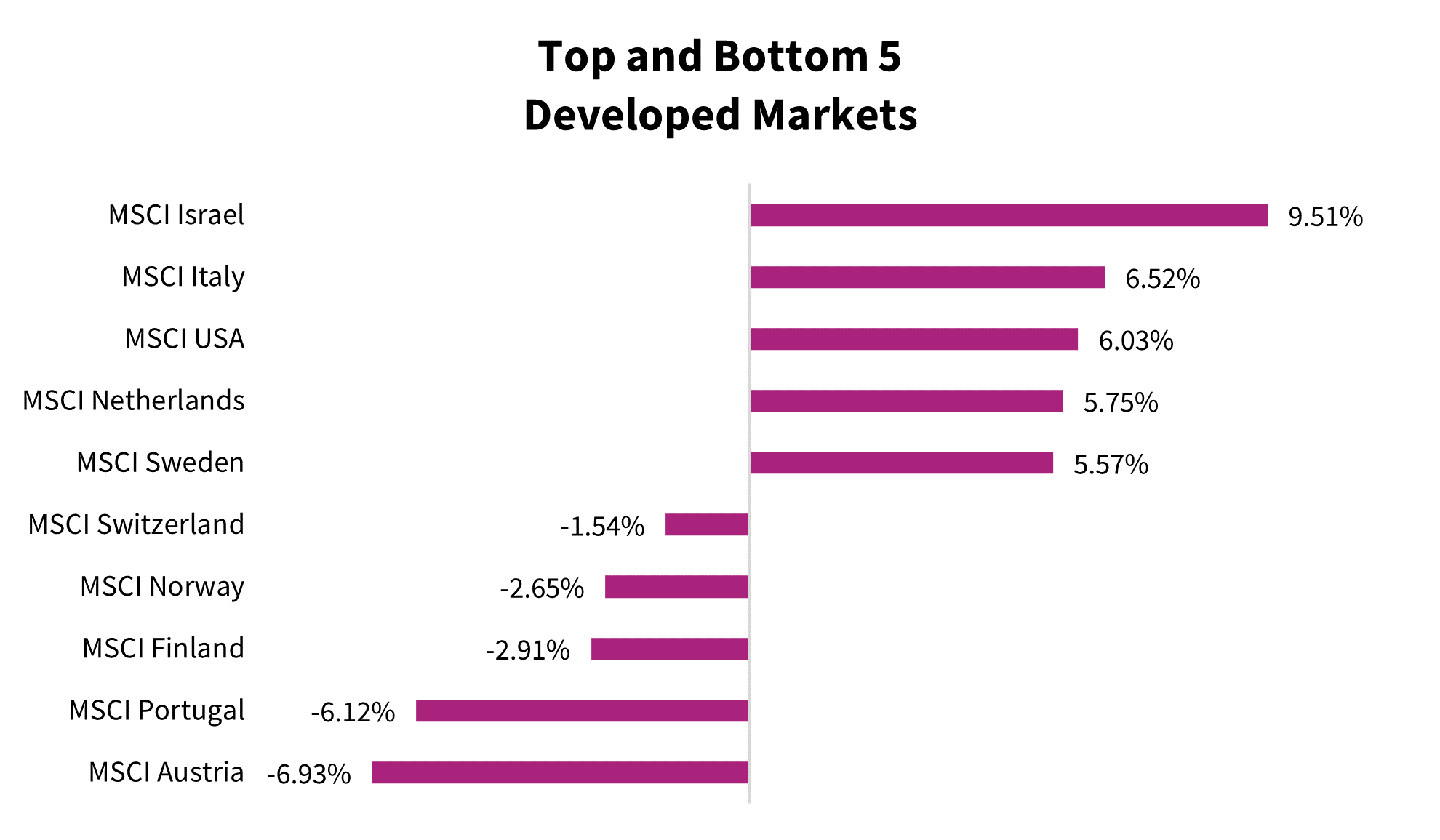

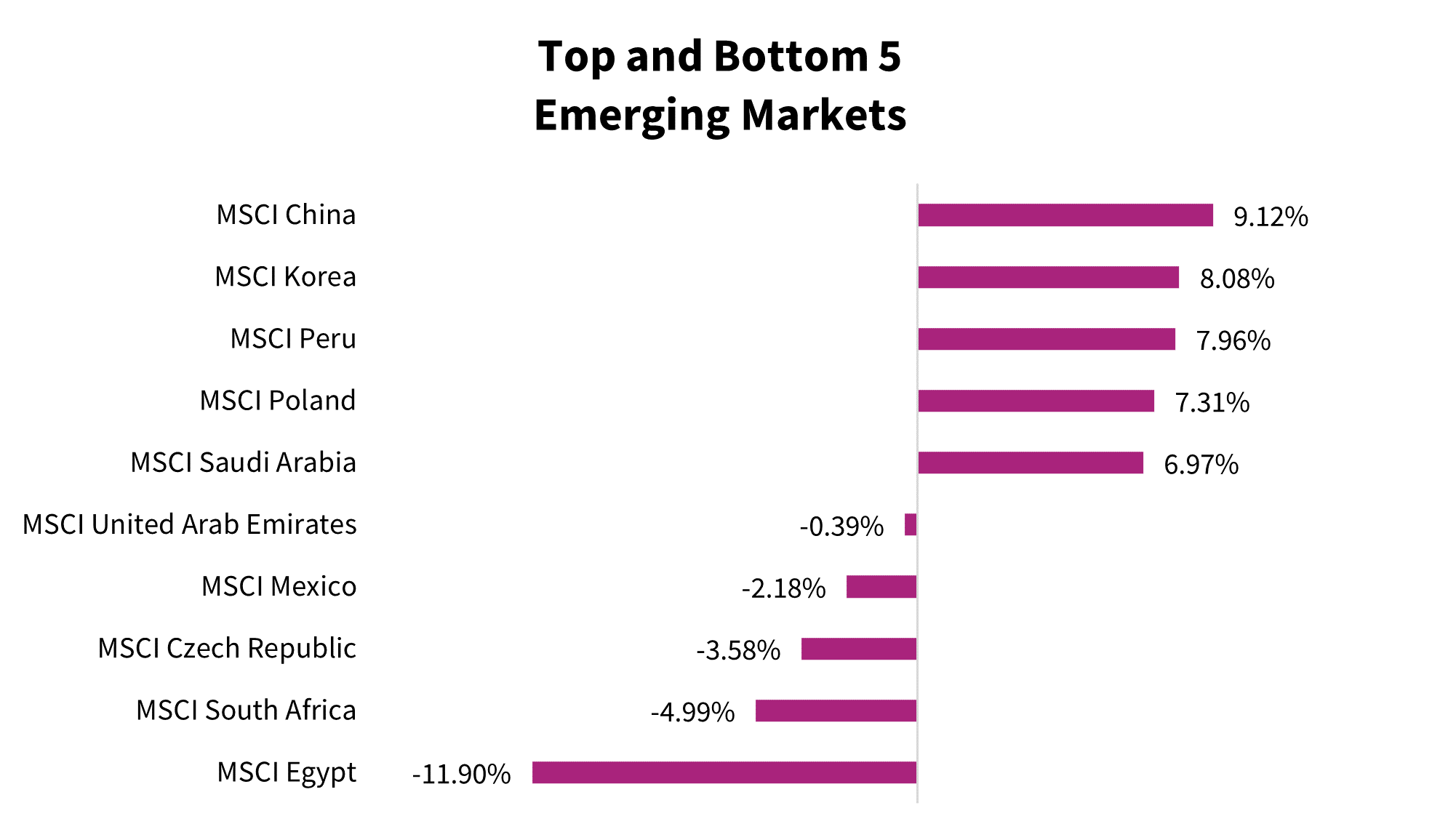

Market performance.

Developed Markets were mixed this month with Israel (9.51%) leading the way as its market enjoys a recovery from recent lows. Elsewhere, Developed Market returns ranged from +/- 6.00% with Italy gaining 6.52% whilst Austria returned -6.93%.

Multinational automotive manufacturer Stellantis helped to drive gains in the Italian market, returning 18.51% for the month. Stellantis is the manufacturer of 14 car brands including Alpha Romeo, Maserati and Peugeot, demonstrating capability in the luxury and ‘every day’ car range.

China enjoyed a strong recovery in February, returning over 9.00%. The market had hit 5 year lows coming into the month but was buoyed by a cut to mortgage rates, stock purchases by state owned enterprises and a curb on short selling. The Chinese market is used to seeing swings of this size so time will tell if this is an inflection point for change or a temporary rebound.

MSCI Egypt fell by almost 12% after enjoying double-digit gains in prior months, again highlighting that swings of this size are normal in this market and don’t necessarily have to be driven by a fundamental catalyst and can simply be driven by ‘mean reversion’.

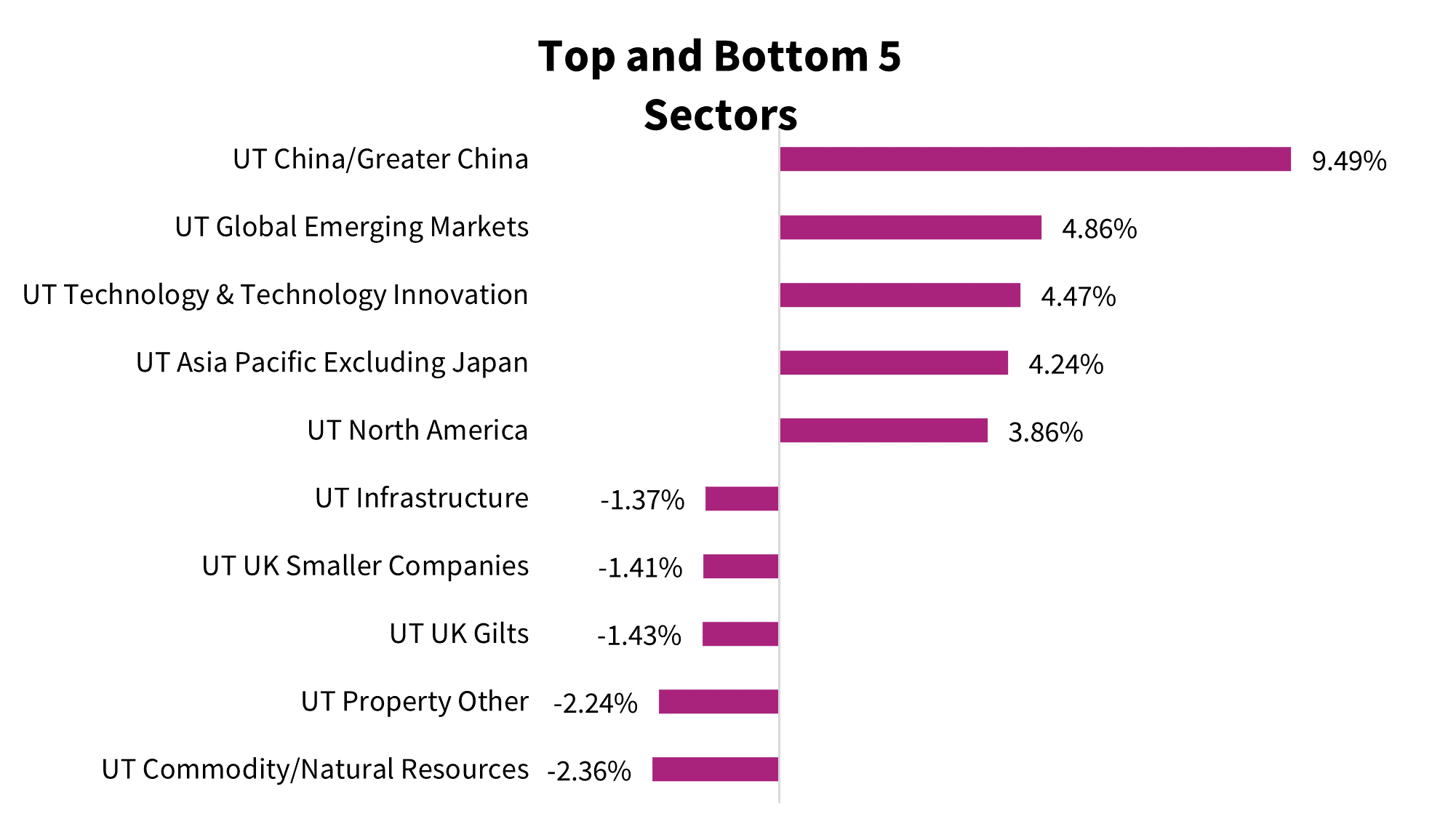

Sector performance.

The theme at market level continued at sector level with China/Greater China adding almost 9.50% and propping up the Emerging Market sector, the gains of which were primarily driven by the Chinese market. At the bottom-end of the scale, Commodities fared less well (-2.36%) as demand flattened out.

Source: FE FundInfo, 09/02/24

Summary.

Large moves in Emerging Markets indices are not unusual at all. In fact, over the last two years, we have seen the MSCI China Index produce monthly returns as high as 25.40% in November 2022, and as low as -19.34% for the month prior. The market will have to wait and see if this time really is different as the state steps in to provide Equity market support through an Equity buying programme and temporarily banning short selling.

The UK is currently in a technical recession, having experienced two quarters of negative growth. One could posit that the restrictive policy implemented by the Bank of England is taking effect in controlling and slowing inflation to a much more palatable level for consumers. The recession is one that all hope is short-lived and shallow and one that is by design, caused by monetary policy.

Odds have shortened and now only 4% of market participants think that the US Federal Reserve will cut rates at their March meeting, compared with 16% at the time of last writing.

Markets seem content with the timing of rate cuts though, as both the S&P 500 (7.09%) and Nasdaq 100 (6.87%) ETF markets have delivered strong returns, year-to-date.

Download

Author: Anthony Walters – Head of ESG at Clever Adviser Technology Ltd (Clever)

Sources:

Economic indicators information from The Institute for Supply Management – Report on business, IHS Markit and Trading Economics

The ‘Balanced Portfolio Benchmark’ is the UT Mixed Investment 20-60% Shares Sector.

Market and Sector performance data sourced from FE FundInfo, 04/03/2024

S&P 500 and Nasdaq 100 data is sourced from ETF versions via FE Fundinfo as at 07/03/24

Bank of England could cut interest rates before inflation hits 2%, Bailey says, by Pedro Goncalves, Yahoo Finance, 20/02/24

Fed’s Powell still expects rate cuts, but inflation progress “not assured”, by Howard Schneider, Reuters, 06/03/24

ECB policymakers push back on hasty rate cuts even as inflation falls, by Reuters, 15/02/24

Important Information:

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from Clever to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. You should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine – together with your own professional advisers if appropriate – if any investment mentioned herein is believed to be suitable. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice.

All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. Issued by Clever Adviser Technology Ltd (Clever), a company registered in England and Wales (company number: 2910523) with registered office at Watergate House, 85 Watergate Street, Chester, Cheshire CH1 2LF.

[/vc_column_text][/vc_column][/vc_row]